Home / Programs / Business Initiatives /

Opportunity Zones

The Federal Opportunity Zones Program was established by Congress through the Tax Cuts and Jobs Act of 2017. The purpose of the program is to promote investment and drive economic growth in low-income and/or economically disadvantaged communities.

Program Description:

The Tax Cuts and Jobs Act of 2017 authorized the governor of each U.S. state and territory to nominate a certain number of qualifying census tracts as “Opportunity Zones.”

Investments made through certified investment vehicles created as “Opportunity Funds” are used to spur economic growth in designated Zones—for example, by supporting new businesses or real estate development. Parties who invest in Opportunity Funds can benefit from tax incentives, such as deferrals on capital gains tax. An Opportunity Fund may be organized as a corporation or partnership whose assets comprise at least 90% qualified Opportunity Zone assets, representing an investment in Opportunity Zones.

Following a statewide application process, the Governor nominated Nebraska’s maximum allowable 44 census tracts for Opportunity Zone designation on March 21, 2018. These nominations were then submitted to the U.S. Department of the Treasury, which administers the program, and were subsequently confirmed on April 9, 2018.

Who Benefits from the Designation of Opportunity Zones?

By driving capital investment and generating economic opportunities, the Opportunity Zones Program benefits individuals, communities, and states. In addition, certain investments made by U.S. investors, e.g., the reinvestment of unrealized capital gains into Opportunity Funds, may benefit from favorable tax treatment and incentives, such as temporary deferrals.

How were Nebraska’s Opportunity Zones Designated?

Under federal rule, each state was allowed to nominate as an Opportunity Zone (a) 25 eligible census tracts or (b) 25% of the total eligible census tracts within the state—whichever was greater. There was not a requirement for states to nominate all eligible census tracts. Nebraska was eligible to nominate a maximum of 44 census tracts under this formula.

Census tracts eligible for nomination included those in which:

- The tract poverty rate was at least 20%, or:

- If located in a metropolitan area, the tract’s median family income did not exceed 80% of the greater of (i) the median family income in the metropolitan area or (ii) the statewide median family income, or;

- If located in a non-metropolitan area, the median family income for such tract did not exceed 80% of the statewide median family income.

The Nebraska Department of Economic Development (DED) distributed information regarding Opportunity Zones and the program application process to city and county officials, economic development organizations, chambers of commerce, business leaders, the media, and other groups in February, 2018. This resulted in DED receiving 34 program applications comprising 107 eligible census tracts. Census tract recommendations were referred to the Nebraska Governor for review and approval. The Governor submitted final tract nominations to the U.S. Treasury Dept. on March 21, 2018. The Treasury Dept. confirmed Nebraska’s 44 tract nominations on April 9, 2018.

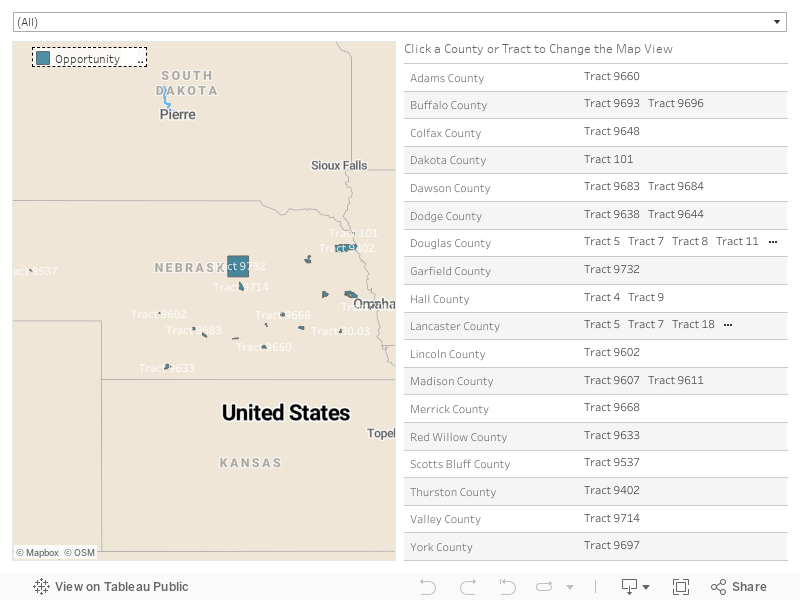

Which of Nebraska’s Census Tracts Have been Designated as Opportunity Zones?

The interactive map and button below list the 44 Nebraska census tracts that have officially been designated as Qualified Opportunity Zones as of April 9, 2018. For a full list of U.S. opportunity zones, click here.

NOTE:

On April 24, 2017, the IRS posted a list of frequently asked questions (FAQs) concerning Qualified Opportunity Zones. This FAQ included a definition of Qualified Opportunity Funds (QOZ); described how to obtain the tax benefits for an opportunity zone; addressed how a taxpayer can become certified as a qualified opportunity fund, and provided other information.

Under the Opportunity Zones program, Treasury is required to issue rules for the certification of QOF — a new class of investment vehicle (organized as a corporation or partnership). The FAQ explains that approval or action by the IRS to certify a QOF is not required, and that eligible QOFs can self-certify. To self-certify, a taxpayer completes a form (to be released during summer, 2018) and attaches it to the taxpayer’s federal income tax return for the tax year.*

*Opportunity Zone investments are made at the sole discretion of Opportunity Zone investment funds and their investors. Opportunity Zone investments are not administered or overseen by DED. Individuals are advised to seek professional guidance when making tax-related decisions.

Questions about Opportunity Zones?